Dear all,

This year, I have moved from UK back to CH and needed to re-open a bank account to receive income. But what banks offer the cheapest services? Personally, I look for very basic things:

- A simple Swiss bank account to receive income

- A Maestro with cashless option

- Online / mobile banking

- As low fees as possible

For all additional services I wish not to pay for. In the end, I will not use any extras (for investing I am using the cost-effective Interactive Brokers).

Previously, I have been with Zürcher Kantonalbank (ZKB) as well as UBS that offered accounts for free since I was a student + a few additional perks such as free use of the night trains in Zurich. While this offer is great for students, I cannot benefit from this anymore as a young professional who started to work. Both UBS and ZKB charge significant annual fees for accounts (~40-60 CHF/year). While this is not drastic, I think it is worth to make a fair comparison among banks to compare if you get the same service for less. This is what I have done here and post here for your reference - and it turns out that changing banks is worth it! Extrapolating to 10 years, you can avoid 60 CHF * 10 = 600 CHF simply by going for a free provider (see below) and getting essentially the same service.

But before the comparison, I would like to shed a light on why banks provide free services to young adolescents but charge them later. This principle is often referred to as a “bait” offering. You provide something for free early, attract young customers with great offers (e.g., using the night trains for free), and then charge afterwards. On the longterm, you are going to pay them significant fees. The reason this is so widespread in banking is that people typically do not change banks. It is associated with effort: You need to inform your employer to use a different IBAN for payments, maybe you have standing orders, time spent closing the old account etc. People typically stick to their bank, even if they pay too much and their offering does not suit individual requirements!. You might think “Hey, it is not that much and I don’t want to bother”, and this is what banks rely on. Nevertheless, significant costs can be reduced when comparing the offering (and this is true for everything: From banks, insurances, flats and all sorts of things) and these costs do add up over time. I highly recommend making comparisons. In the end, it is also about promoting healthy competition: Why not reward innovation / better services? If everyone simply sticks to a service forever, there is little incentive to get better at all or to pass on cost savings to customers.

Now, find below a comparison table of bank providers (data as of 26.12.19). The clear winner for me is CLER bank! I looked for the 10 largest banks and researched their principal costs (annual account fees, card fees and the like). I excluded Julius Bär as private bank (they do not seem to offer simple accounts and focus more on investing):

| Bank | Annual account fees | Card fees (for Maestro card) | Interest rates | Other | Source |

|---|---|---|---|---|---|

| UBS (private account) | 36 CHF (if statements delivered digitally + >10k CHF on the account), otherwise: 60 CHF | Fee not disclosed | 0% | N/A | Click here |

| Credit Suisse (private account) | 60 CHF | 50 CHF | 0% | N/A | Click here |

| Raiffeisen (private account) | N/A | 40 CHF | 0% | Account closure: 15 CHF | Click here |

| Zürcher Kantonalbank (private account) | 12 CHF | 40 CHF | 0% | N/A | Click here |

| Postfinance (basic private account) | 60 CHF (as of 2019) | Free | 0% | N/A | Click here |

| Banque Cantonale Vaudoise (“direct account”) | 42 CHF (first 6 months free) | Free | 0% | N/A | Click here |

| Basler Kantonalbank (private account | 60 CHF (if <10k CHF on account), otherwise: Free | 50 CHF | 0% | Account closure: 10 CHF | Click here |

| Luzener Kantonalbank (e-private account) | 50 CHF | 40 CHF | 0% | Account closure: 20 CHF | Click here |

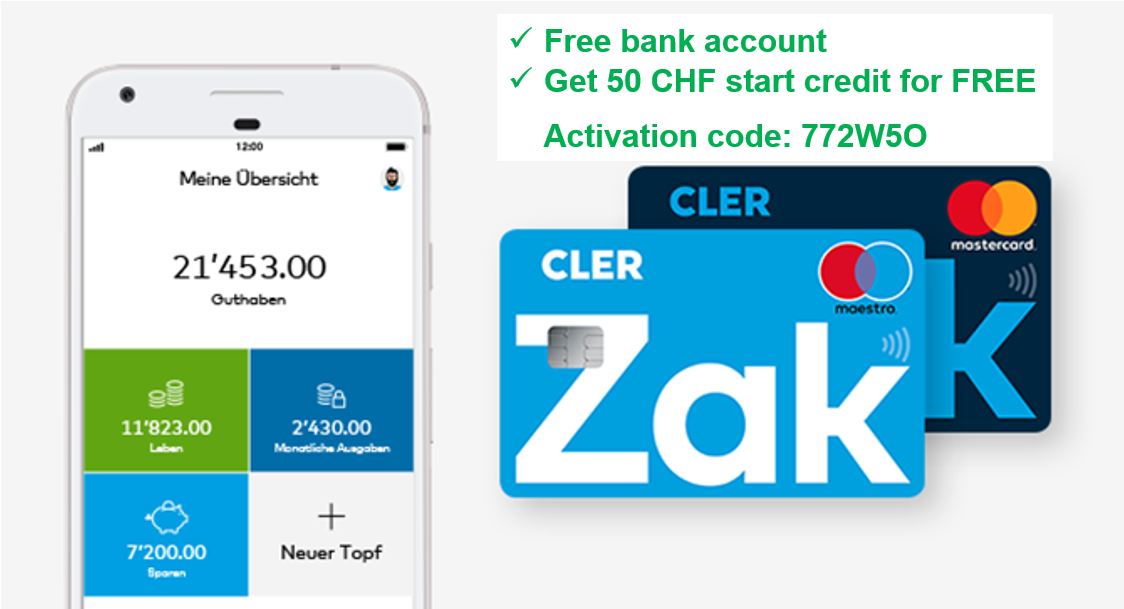

| Cler (ZAK account) | 0 CHF | 0 CHF | 0% | Opening an account is rewarded with 50 CHF | Click here |

Unsurprisingly, interest rates are at 0% so it really comes down to cost. Opening the accounts were 0 CHF throughout and is not a differentiating factor. With annual fees for holding the account and (often mandatory) fees for getting a maestro card (/same or higher costs for credit cards) the picture is clear: Cler is the least expensive service. One should always consider other less direct costs too, such as the cost for transactions (see Migros), withdrawing money (if you often withdraw money and use cash, then large banks with many ATMs such as UBS are favorable) or (monthly) paper statements. Personally, I prefer to use my Card so for me the number of ATMs is less important. Worthy of note is PostFinance, which has offered free accounts until 2019. They have changed their policies leading to many people (including me) to change provider.

I have been using Cler for a full year now, and I can tell you that my effective costs are 0. There are no “hidden” costs. Additionally, since they are attracting new and more customers, you will receive 50CHF for free if you open an account with them. There is no hidden issues, it is simply an effort to grow and attract customers (remember what we said earlier? Attracting customers is extremely difficult because people generally stick to their banks!). I can highly recommend ZAK, it has all the basic features I was looking for:

- Free maestro and free credit card (both with cashless function)

- No annual account fees

- Overall ZERO annual cost

- Mobile banking Of course there is more but this but this is the essentials. As with other banks, you want to make sure to tick the box saying you do not want to receive monthly paper statements and instead receive them on your account (to save the environment AND avoid costs).

Another nice feature is that you can refer your friends. This way, you AND your friend receive 50 CHF. So if you are curious I would be extremely thankful if you would use my referral code and we will BOTH benefit from 50CHF: 772W5O

Please note: I would NOT recommend it if I would not be 100% convinced of CLER. I absolutely love it and only therefore recommend it. In fact, I also recommended it to my girlfriend and a growing numbers of our friends are adopting it too (especially previous PostFinance clients). Afterwards, you can also refer your friends and continue to receive 50CHF which is a nice perk!